Top>Opinion>Active Learning as Liberal Arts Education: Cases of “Program for Experiencing Business Formation”

Index

Index

Active Learning as Liberal Arts Education: Cases of “Program for Experiencing Business Formation”

Sumitaka Ushio

Associate Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Management Accounting, Accounting Education

Introduction

Recently, an approach called active learning (AL) has been drawing attention in contrast to lecture-style learning. As part of such an initiative, my seminar class implemented the “Program for experiencing business formation” (Tobita, 2014) to experience the series of processes related to the stock company system, management and accounting including the establishment of a mock company, financing, business activities, accounting audits, dividends and company liquidation through refreshment stands at school festivals. In the following sections, I will explain such initiatives and present my personal opinion about the significance of AL.

Outline of the Program for Experiencing Business Formation

The program works in the following way (for details, see Ushio (2016)). First, after lectures on the stock company system, company management, finance and management accounting, students establish a mock stock company by preparing the articles of incorporation and completing the registration (around September). At this point, the students contribute only the funds required for prior procedures to open a stall. Next, students call on partners outside the university (to be explained later) to explain the purpose of the program and request participation in the investment (capital increase) briefing (around October). Students present and explain the business plan to the partners who have participated in the capital increase briefing, and issue shares in accordance with the terms and conditions finally agreed upon. Using the funds collected, students operate the stall for four days during the school festival (Hakumon Festival). Students keep records of all transactions and prepare financial statements including the balance sheet and statement of income. Furthermore, after undergoing an audit by a certified public accountant and the general meeting of shareholders, they pay dividends and liquidate the company (around December).

Partners outside the university in FY2015 included people with various careers such as management consultant, manager at a global company, education-related careers, as well as students from other universities. While many of them are my friends, they were not informed of the details of the request. Although many students came hours late for the volunteer seminars in the beginning, we saw them engaging in earnest discussion with textbooks in their hands just before their visits to partners (in August).

Business Plan and Earnings of the “TAISAN Co. Ltd.”

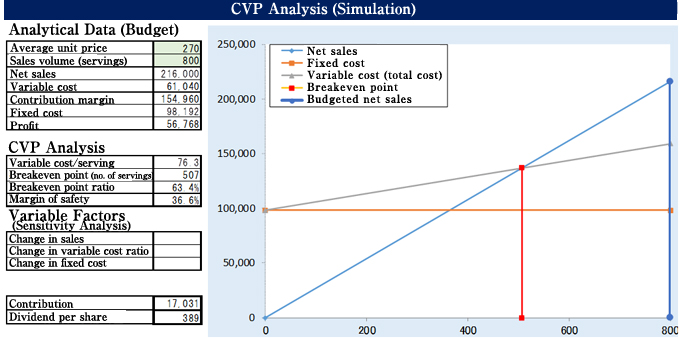

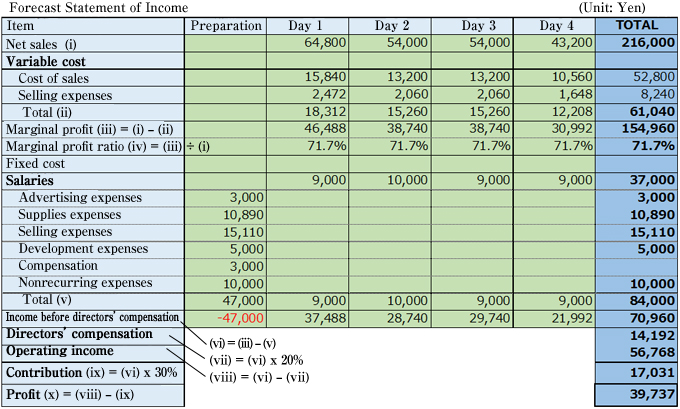

Figures 1 and 2 show the cost-volume-profit analysis (CVP Analysis) and the forecast statement of income for which TAISAN Co. Ltd., mainly engaged in the production (hand-made) and sale of dumplings, included in the business plan as a “promise to shareholders.” After conducting research on the situation of other companies, they forecast sales of 216,000 yen for 800 servings and net profit of 39,737 yen for the total of four days. “Salaries” of 37,000 yen (fixed amount) and directors’ compensation of 14,192 yen (performance-based) represent the total of the distributions to the 11 founding members (all of whom were directors). “Contributions” equivalent to the income tax for real companies was uniquely established as a management rule for this program.

Figure 1 CVP Analysis in the Business Plan

Figure 2 Forecast Statement of Income in the Business Plan

In the advance individual briefings and capital increase ones, we received various opinions from outside partners (candidates for shareholders), including: “If you want to make profit, you should use frozen dumplings instead of hand-made ones”; “If you do something, you should try something different which will bring excitement to the university festival”; “Are you going to get paid even if this is something you are doing for your coursework?”; and “Will you pay so much in dividends?” (in the business plan, a dividend of 389 yen is assumed for the capital contribution of 1,000 yen for one share). They cannot conduct business if they accept all of these opinions. They must make their choices based on their own thinking. About half of the initially expected number of people ultimately agreed to make capital contributions, and with 84,000 yen in hand including the 22,000 yen they contributed at the time of establishing the company, they began conducting business.

Atmosphere of the Hakumon Festival

They also had to make numerous decisions afterwards. When they tried to make dumplings despite being inexperienced at cooking, they failed repeatedly due to elementary errors. Until they acquire the minimum basic skills, they may have to practice by purchasing materials with their own, not company, money (development expenses).

With the assumption of using Chinese cabbages from Ibaraki prefecture which suffered from floods just before the festival, their business plan emphasized that it would be part of their activities to contribute to society. However, just before the Hakumon Festival, it turned out that such cabbages could not be purchased at nearby supermarkets, and it would require huge shipment costs to purchase them directly from the producing areas. Which should be given priority, the target profit or use of cabbages from Ibaraki prefecture?

When the Hakumon Festival started, they could not sell at all because their products were not known. Some students walked around campus the whole day, unsuccessfully soliciting visitors; some bought dumplings themselves; or, thinking that would be nonsense, some proposed to acquaintances at other stalls that they buy dumplings if they won at rock-paper-scissors (and vice versa if they lost). Should the target profit presented in the business plan as a promise to shareholders be achieved even paying with their own money? I saw them discussing this throughout the night during the Hakumon Festival.

In the end, presumably due to the improved taste of the dumplings, which became more popular after repeated trials, sales exceeded the target for two days in the second half (Saturday and Sunday), with sales and profit reaching slightly less than those in the business plan for the total for the four days (photos) (Figure 3).

Significance of AL

In AL in cooperation with outside practitioners including this program, we sometimes start by teaching how to use document and spreadsheet software, how to write emails, and how to accept business cards. It would be dangerous if students were satisfied with feeling like “becoming adults” after acquiring these general skills. It is the most efficient for the knowledge and abilities immediately useful when working for companies to be acquired through practical experience. It would be meaningless if AL merely became their “inferior version.”

The focus of this program is to experience management in its totality, by deciding the products and services which will become the core of the business, formulating the business plan by discussing it with prospective shareholders, and receive their capital contribution. After opening the stall at the Hakumon Festival, they prepared financial statements, discussed their reliability with the certified public accountant, and received approval at the general meeting of shareholders.

As a result of making every effort to fulfil their promise to shareholders, they were able to pay dividends of 380 yen for a capital contribution of 1,000 yen. On the other hand, students worked hard for salaries and compensation which were lower than what they get from their usual part time jobs, while consumers and counterparties such as acquaintances and junior students from their personal connections went out of their way to buy dumplings. How should they assess such results? What did shareholders expect in making their capital contributions? Were they able to meet their expectations? For whom does a company exist? Students can think about and discuss the essential issues for management more closely and with a sense of reality precisely because they have made their own decisions repeatedly in this program which condenses the sequence of processes for managing companies.

For example, you dine with your acquaintances at a restaurant. If you know something about art, you may be interested in the decor and music in the store. Or if you are interested in history and culture, you may pay attention to the origin of the restaurant’s name, or the locality of the ingredients. Similarly, the students who have experienced this program should be able to discuss naturally such things as the location and management of the store, appropriateness of prices, products, and services, ideal employees and managers, and significance of the work.

For many employees who work in companies, shareholders are very distant, and they may have few opportunities to think about the essence of management. What universities should aim at is a liberal arts education to provide opportunities and materials for students to think independently about the essence of things. I am of the opinion that AL is an effective tool for such purpose.

References

- Tsutomu Tobita (2014) “The Case of Accounting Education through a Refreshment Stall: Initiative for Experiencing Business Formation at Faculty of Commerce, Fukuoka University [Mogiten-shutten wo tsujita kaikei kyoiku no jirei: Fukuokadaigaku Shogakubu ni okeru sogyotaiken puroguramu no torikumi),” Journal of Accounting Education and Research [Kaikei kyoiku kenkyu] 2, pp. 32-40.

- Sumitaka Ushio (2016) “Pursuit of Issues in Accounting Education in the ‘Program for Experiencing Business Formation’: Ethnography [‘Sogyotaiken puroguramu’ ni okeru kaikei kyoiku no ronten tankyu: esunogurafi],” Journal of Accounting Education and Research [Kaikei kyoiku kenkyu] 4 (to be published soon).

-

Sumitaka Ushio

Associate Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Management Accounting, Accounting Education - Associate Professor Ushio was born in Osaka in 1979. He graduated from the Faculty of Economics, Kyoto University, and earned an MIT Diploma in Communication Studies at Manukau Institute of Technology (NZ). Before assuming his current position, Professor Ushio worked for Sony Corporation in the Accounting Department ; completed Master’s and Doctoral programs at the Graduate School of Economics, Kyoto University; and served as a lecturer and associate professor in the School of Management, Chukyo University. He has a doctor’s degree in economics from Kyoto University.

- Research Activities as a Member of Research Fellowship for Young Scientists (DC1), Japan Society for the Promotion of Science (JSPS) Shuma Tsurumi

- Important Factors for Innovation in Payment Services Nobuhiko Sugiura

- Beyond the Concepts of Fellow Citizens and Foreigners— To Achieve SDGs Goal 10 “Reduce Inequality Within and Among Countries” Rika Lee

- Diary of Struggles in Cambodia Fumie Fukuoka

- How Can We Measure Learning Ability?

—Analysis of a Competency Self-Assessment Questionnaire— Yu Saito / Yoko Neha - The Making of the Movie Kirakira Megane