Top>Opinion>Misunderstanding in Discussions on Reduced Tax Rates

Index

Index

Toshiaki Hasegawa【profile】

Misunderstanding in Discussions on Reduced Tax Rates

Toshiaki Hasegawa

Professor, Faculty of Economics, Chuo University

Areas of Specialization: International Economic Policy, Interindustry-Based Macro Econometric Modelling

A system design as a forgotten anti-poverty measure

According to a survey by the Ministry of Internal Affairs and Communications, the real disposable income of households in Japan (workers’ households with two or more persons) in 2014 decreased by 70,000 yen to less than 410,000 yen from the peak average monthly income in 1997, representing the lowest amount in the past 30 years. The real disposable income is calculated by subtracting non-consumption expenditures such as direct taxes and social security contributions from the actual income, and then discounting the effect of price changes. Among the real disposable income, the ratio for consumption (the average propensity to consume) has reached as high as 75% now.[1]

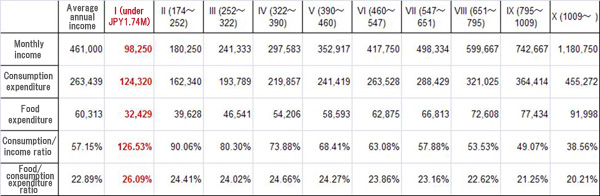

Against the average monthly households disposable income of 405,000 yen for such workers, the portion directed to consumption expenditure is 310,000 yen, of which 74,000 yen is spent on food. This is the actual situation of the average worker’s household today.[2] On the other hand, with such a standard of living, relatively poor people—who are regarded as the vulnerable unable to enjoy the affluence of society—account for 16.1% of the Japanese population, according to the figures published by the Ministry of Health, Labour and Welfare and the OECD. As for the household income of the lowest decile according to annual income, the statistics for 2014 are to be published this month, but are not available as of this writing. Looking at the most recent data available (2009), households with an annual income of 1.74 million yen or less belonging to the lowest decile, show regular deficits with consumption expenditure being 1.26 times their income every month. For those who are living below the poverty line, how effectively have we developed social security systems and measures in Japan? Should we not demand that our government develop systems of inclusive and sustainable anti-poverty measures?

Table 1 Average of Monthly Disbursements per Household by Yearly Income Decile Group (2009) (Unit: Ten thousand yen)

Source: Prepared from Ministry of Internal Affairs and Communications E Stat, “2009 National Survey of Family Income and Expenditure”

The anti-poverty measures in the U.S. guarantee basic food expenditure, while there are differences in the system. The annual income of four-member families living below the poverty line, accounting for almost the same about 16% of the population as in Japan, was 2.86 million yen in 2014. For the income group defined as below this poverty line, each member of a family receives 125 dollars, or 15,000 yen (calculated at the current exchange rate of 120 yen/dollar) every month in his/her debit card automatically through EBT (Electronic Benefits Transfer). Since June 2014, all states have introduced this EBT, whose card enables the purchase of food. For the purchase of food, 60,000 yen is given to four-member families which account for 16% of the population.

My basic idea is that the current discussions on reduced rates based on the single year budget focusing on financing—saying that a budget of approximately 500 billion yen will be necessary if we provide the amount calculated by multiplying 4,000 yen per person and the population together—will not give relief to the socially vulnerable as originally intended. Is it a preferable system of consumption tax which is likely to re-ignite the issue of increasing ad hoc benefits at a time of probable further increase in consumption tax rates?

The root of financing discussions for reduced tax rates

From the Family Income and Expenditure Survey of the Ministry of Internal Affairs and Communications, we can obtain the statistics appropriate for the discussion here—those on household consumption by expenditure items which classify consumption expenditure into basic consumption expenditure and selective consumption expenditure.[3] This basic consumption expenditure is what should be regarded as the required level for maintaining the minimum standard of living for citizens. Among the basic consumption expenditure items, food has been the focus of discussions as the most basic one at the Research Commission on the Tax System of the ruling parties as to whether we should keep its rate of taxation at 8% when the consumption tax rate is raised to 10%.

The issue—of guaranteeing the vulnerable such basic consumption expenditure within the single-year national budget—has been almost completely missing from the discussion elsewhere. In Europe where a standard value added tax of 20% is levied, the system is structured so that uniform reduced tax rates are applied on the basic consumption expenditure regardless of income level, while those who make selective consumption expenditure are made to bear the burden in order to secure the financing of social security. It is a failure to see the forest for the trees to say that reduced rates are a major problem because they also benefit high-income earners. That is because the income groups which make selective consumption expenditure are the ones to provide necessary financing. If we compare income groups in deciles or quintiles, there is not much difference in the basic consumption expenditure made by the high income group and low income group. On the other hand, we should turn our attention to the payment of consumption tax on selective consumption expenditure of the high income group, in comparison to those who have difficulty in making even selective consumption expenditure.

How much annual expenditure is necessary for social security? A rough estimation for the necessary budget to help the socially vulnerable and poor can be obtained by multiplying the number of the vulnerable and poor—who cannot afford to pay for basic consumption expenditure on their own—with the average shortfall in income for the basic consumption expenditure. In providing for the medium-term fiscal base in the future, an increase in the standard consumption tax rate will be a choice we cannot avoid. If the consumption tax is raised by 1%, it will increase the tax revenue from the consumption tax by 1.28 trillion yen (CHERP Hasegawa estimate). The base for our social system will be shaken if we hesitate to secure necessary financing by raising the standard consumption tax.

As for the technical issues related to introducing reduced tax rates, the invoice method and the simplified declaration method have been discussed. From the long-term perspective, I have been of the opinion that in order to introduce the invoice method with expected transparency, during the process of developing the institutional infrastructure, it would be preferable to adopt a compromise of applying it only to large-scale businesses for the time being, while applying the simplified method to businesses below a certain threshold of sales as a transitional measure to reduce social confusion.

What is the cause of the confusion surrounding the discussion on reduced tax rates? In my opinion, the problem has been that while we needed to raise the standard consumption tax rate to give such relief to the vulnerable, politicians in the ruling and opposition parties alike—in their efforts to win elections—have been acting irresponsibly by not proposing reform to ask Japanese people to bear burdens, and neglected to secure long-term and stable financing for social security. We should criticize the fact that they have imposed the result of such negligence on the vulnerable. I do not doubt that the Japanese public expected the commitment to social security in exchange for their sharing burdens when the Comprehensive Reform of Social Security and Tax was proposed to them and the draft bill was passed by the Diet.

Notes

- ^ Statistics Bureau, Ministry of Internal Affairs and Communications, “Family Income and Expenditure Survey - Total Households: Outline of Preliminary 2014 Yearly Average Survey Results” February 17, 2015

- ^ The National Survey of Family Income and Expenditure was published by the Statistics Bureau of the Ministry of Internal Affairs and Communications in 1999. The 2014 version is scheduled to be published, while part of it is already available. What is used here is the “Average of Monthly Receipts and Disbursements per Household” from the Ministry of Internal Affairs and Communications, Family Income and Expenditure Survey (Total Households) Preliminary report dated October 2015 (published on November 27, 2015). Unfortunately, the comparison of household receipts and disbursements by income deciles is from 2009.

- ^ An expenditure item whose ratio of change is greater than that of basic expenditure, consumption expenditure—i.e., the former ratio divided by the latter is greater than 1.00—is called selective expenditure. Basic expenditure includes food, housing, fuel, light & water charges, and medical care, while selective expenditure includes education, culture and recreation, durable goods (personal computers, etc.) and monthly tuition fees.

- Toshiaki Hasegawa

Professor, Faculty of Economics, Chuo University

Areas of Specialization: International Economic Policy, Interindustry-Based Macro Econometric Modelling - Professor Hasegawa was born in Hokkaido in 1948 and graduated from the doctoral course of International Economics at the Graduate School in Keio University.

Professor Hasegawa has been an associate professor with Takushoku University; a visiting scholar for the Department of Economics and the Center for International Affairs at Harvard University and Brandeis University; a visiting professor for People's Republic of China Shaanxi College of Finance and Economics, Peking University, and Tsinghua University; an instructor for the Customs Training Institute and the Finance Institute at the Ministry of Finance; and a part-time lecturer at International Christian University and Yokohama National University. Currently he is a professor for the Faculty of Economics, Chuo University. - [Affiliation]

The Japan Society of International Economics, the American Committee on Asian Economic Studies

Pan Pacific Association of Input-Output Studies (PAPAIOS), the Interindustry Forecasting Project at the University of Maryland (INFORUM)

The International Input-Output Association - [Recent major publications]

The Craft of Economic Modeling by C. Almon, co-translator, Nippon Hyoronsha, April 2002

APEC Market Integration [APEC no shijo togo], author and editor, Chuo University Press, 2011

“Asia’s Industrial Structure and Interdependence [Ajia no sangyokozo to sogoizon],” co-author, Input-Output, Vol.20, No.1, 2012

3.11 Complex Disaster and Challenges for Japan [3.11 Fukugo-saigai to nihon no kadai], co-author, Chuo University Press, 2014

- Research Activities as a Member of Research Fellowship for Young Scientists (DC1), Japan Society for the Promotion of Science (JSPS) Shuma Tsurumi

- Important Factors for Innovation in Payment Services Nobuhiko Sugiura

- Beyond the Concepts of Fellow Citizens and Foreigners— To Achieve SDGs Goal 10 “Reduce Inequality Within and Among Countries” Rika Lee

- Diary of Struggles in Cambodia Fumie Fukuoka

- How Can We Measure Learning Ability?

—Analysis of a Competency Self-Assessment Questionnaire— Yu Saito / Yoko Neha - The Making of the Movie Kirakira Megane