Top>Opinion>Finance Theory for Investment

Index

Index

Hiroshi Ishijima [Profile]

Finance Theory for Investment

Hiroshi Ishijima

Associate Professor, Chuo Graduate School of International Accounting, Chuo University

Areas of Specialization: Finance Theory and Financial Engineering

Finance means raising and investing money. Specifically, finance is to model the flow of money in fundraising and investment-the cash flow-in chronological order, and evaluate, control, and measure it by using information. Finance theory is the discipline for studying this process. Among subjects treated in finance theory, I am especially engaged in investment, corporate analysis and evaluation, and real estate. In this essay, I will introduce studies on investment.

1. Investment games were the mother of probability theory and quants

Determining whether or not there is a winning strategy for investment, or for how to make a profit, provides motivation for taking an interest in finance. To give the conclusion up front, such a theory exists. Probability theory, a field in mathematics, originated when Cardano and Pascal studied winning strategies for card games in the 16th and 17th centuries. In the 20th century, Black, Scholes, and Merton exploited tools of stochastic calculus introduced by Bachelier and Kiyoshi Ito and built the theoretical background of derivatives and other financial vehicles since the 1970s. Combined with the establishment of open markets for such products, complex and sophisticated financial markets have been expanding to date in a borderless fashion. This, then, has led to the advent of so-called quants, highly specialized professionals with skills of freely utilizing them. Thorp, who was a professor of mathematics at the University of California, is called the godfather of quants.

2. Gambles and information theory

Thorp initially worked out a winning strategy for blackjack, a card game still popular in casinos, in which a player wins when her cards in hand total 21. Together with Shannon, who was also a founder of information theory, Thorp is said to have carried the world's first wearable computer (mobile PC) into a casino to predict roulette outcomes. If he had continued winning, however, he would have become well recognized in the casino. Therefore, he had to spend significant amounts in order to disguise himself. Reportedly, he was even in physical danger eventually (interested readers should watch the 2008 film, 21![]() ). So, Thorp gave up the casino and started investing in the stock market. He then operated his own hedge fund successfully to the extent that he was called the godfather of quants (see, for example, Patterson, The Quants

). So, Thorp gave up the casino and started investing in the stock market. He then operated his own hedge fund successfully to the extent that he was called the godfather of quants (see, for example, Patterson, The Quants![]() , 2010).

, 2010).

3. The winning strategy for investment: the optimal growth portfolio strategy

Now, what was the winning strategy for investment behind Thorp's American dream? Simply put, it was to represent the cash flow generated by investment targets in a probabilistic form and implement a strategy that would maximize the expected growth rate of invested money. This strategy is called the optimal growth portfolio strategy. Investors do not have to even know the precise probability of winning in the investment. The strategy for learning such a probability to achieve optimal growth is called the universal portfolio strategy. I analyzed whether those two strategies could actually achieve the goal. Indeed, they work well with constantly growing markets. They do not show good performance, however, when they are directly applied to markets that remain in a stagnant and chaotic state, such as the Japanese stock market since the 1990s.

4. How to determine the timing for investments

Now, let us consider the following. The stock market is not always sluggish, but rather it is in turmoil, repeating upward and downward phases. Therefore, when you buy stocks at the beginning of a rising period and sell them at the onset of a declining one, you will find an opportunity to make profit. Wait for the time of a good opportunity, and when you find a signal, multiply your investment based on the optimal growth strategy-this is the winning theory for investment known in the academic realm. In blackjack, you should count the cards placed on the table so far to observe the timing. In a financial market, observe the underlying invisible economic conditions, or the timing when the regime switches from a strong economy to a weak one, or vice versa. Keiki is a Japanese word associated with economic upturns and downturns-dating back at least to Hojoki written by Kamo no Chomei in 1212-which originally meant the mood or color in the sky. In other words, it depicts something invisible. Estimate it as the probability that the economy is in a boom or a recession. This is, in a sense, a business forecast. Based on this forecast, exercise the optimal growth strategy while watching for the timing of investing more funds in stocks during an upswing and in bonds during a downswing, for example.

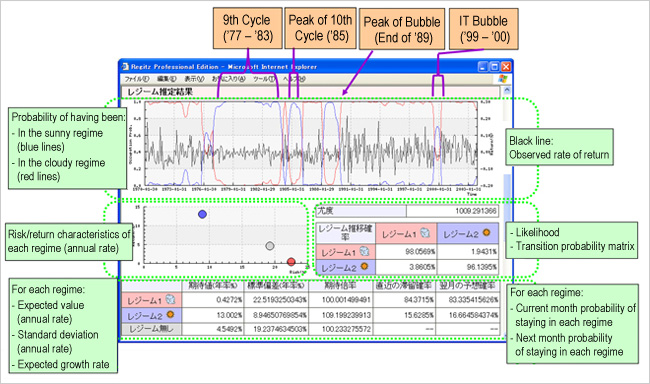

5. Development of the investment system Regitz

In order to achieve investment that exploits such timing, we developed an asset management system called Regitz (see figure). The concept is to make the system available to everyone on the web in order to contribute to creating a rich and hopeful society going forward. The name Regitz is derived from letters selected to be suitably pleasing to the ear, from the sentence: Comprehensive Asset Management System subject to Regime Switching, Based on Information Technology in honor of Harry Markowitz, who is a pioneer of portfolio theory. The prototype was completed with support from the Information-Technology Promotion Agency, Japan, though the support is currently shelved, unfortunately.

Here I introduced a subject in finance that I am engaged in. I would be happy if readers took this opportunity to take an even the slightest interest in finance, and decide to study finance at Chuo University. It would also be our pleasure if those who became interested in financial studies at Chuo University offered us cordial assistance.

Example of Regitz screen:

Business forecasts for investment targets are automatically conducted on the web. Whether it will be sunny (high-return-low-risk) or cloudy (low-return-high-risk) tomorrow is stochastically predicted, and rewards and risk exposure are calculated for each of those stochastic scenarios.

- Hiroshi Ishijima

Associate Professor, Chuo Graduate School of International Accounting, Chuo University

Areas of Specialization: Finance Theory and Financial Engineering -

Mr. Ishijima is Associate Professor, Chuo Graduate School of International Accounting, Chuo University. He graduated from a doctoral program at Tokyo Institute of Technology (Doctor of Engineering, 1999). Before assuming his current position, he worked on the Faculty of Policy Management, Keio University Shonan Fujisawa Campus; at the Center for Finance Research, Nihonbashi Campus, Waseda University; and the Center for the Study of Finance and Insurance (CSFI), Osaka University. At CSFI, he was concurrently a part-time lecturer. He specializes in finance theory and financial engineering. Apart from academic papers, his publications include Valuation Map: the Science and Practice of Corporate Evaluation [Baryue-shon Mappu: Kigyo Kachi Hyoka No Kagaku To Enshu] (Toyo Kezai, 2008)*. Professor Ishijima was awarded the first Best Paper Award from the Japan Academic Society for Financial Planners in 2010; the Award for Excellence at the Academia/Technology & Solution Session 2010 of the SAS User Conference in 2010; and the Prize for Encouragement of Academic Research from Chuo University in 2011.

Valuation Map [Baryue-shon Mappu]*

Website:http://ilabfe.jp

* This textbook describes corporate analysis and evaluation, one of the author's research and education fields. This subject is systematically taught at the Chuo Graduate School of International Accounting (CGSA), which strives for the convergence of finance and accounting.

- Research Activities as a Member of Research Fellowship for Young Scientists (DC1), Japan Society for the Promotion of Science (JSPS) Shuma Tsurumi

- Important Factors for Innovation in Payment Services Nobuhiko Sugiura

- Beyond the Concepts of Fellow Citizens and Foreigners— To Achieve SDGs Goal 10 “Reduce Inequality Within and Among Countries” Rika Lee

- Diary of Struggles in Cambodia Fumie Fukuoka

- How Can We Measure Learning Ability?

—Analysis of a Competency Self-Assessment Questionnaire— Yu Saito / Yoko Neha - The Making of the Movie Kirakira Megane