Using Tax Data to Conduct Analysis of Income Distribution of High-income Earners

Shigeki Kunieda/Professor, Faculty of Law, Chuo University

Area of Specialization: Public Finance and Macroeconomics

Heightened interest in the increasing income disparity

The growing income disparity is attracting attention in every country. This awareness was spurred by Capital in the Twenty-First Century, a best-selling book authored by Professor Thomas Piketty, which pointed out how income has been concentrated in the super-rich class in advanced nations since the mid-1980s. This point is founded on analysis of income distribution based on tax data in each country. Analysis of income distribution in the past often used a type of household survey data, but in most cases, it did not include a sample of the super-rich class. On the other hand, tax data contains data from taxpayers, including the super-rich class. However, tax data is a personal information that requires special handling and many countries have imposed strict constraints on the use of tax data from the perspective of protecting privacy. Although, in recent years, an increasing number of countries have allowed academic use of tax data. Researchers such as Professor Thomas Piketty, Professor Emmanuel Saez and the late Professor Anthony Atkinson have actively analyzed this tax data. One result of such analysis was the aforementioned book. Conversely, Japan has not permitted the use of tax data for a long time, and it has been difficult to conduct highly-precise research on income distribution.

Start of academic use of tax data in Japan

However, in June 2021, the National Tax Agency decided to provide researchers with data on income tax returns and corporate tax returns in the form of joint research with the National Tax College, and recruited researchers to participate in the study. Fortunately, my research group was selected as a partner for joint research on income tax return data. We began joint research from April 2022. In this joint research, researchers are assigned as visiting professors at the National Tax College and are given the obligation of confidentiality as defined in the National Public Service Act. Additionally, tax data provided by the National Tax Agency is in a format that gives full consideration to the privacy of taxpayers; for example, the data has been anonymized and is only available for use in a single room in the National Tax College.

The tax data provided in this joint research is panel data for income tax returns over the seven-year period from 2014 to 2020. This is big data consisting of the data of approximately 24 million taxpayers per year. Although the data of taxpayers whose tax procedures are done completely via their withholding tax is not included, taxpayers with a total income of more than 20 million yen are required to file a tax return, so all such taxpayers are included. On the other hand, the certain types of income such as interest income and dividend income subject to separate withholding tax are excluded. Since tax data has not been subject to academic use thus far, my research group has cooperated with the National Tax Agency and spent time organizing the data so that it becomes suitable for academic use.

Income distribution of high-income earners in Japan and the Pareto coefficient

It is well known that the income distribution of high-income earners follows the Pareto distribution. One of the parameters of the Pareto distribution function is called the Pareto coefficient. When the Pareto coefficient is low, it means that the income is concentrated in the high-income class, particularly among the super-rich class that has a particularly high income. For example, an analysis conducted in the United States by Professor Saez et al. in 2007 before the collapse of Lehman Brothers estimated the Pareto coefficient for total income (capital income and labor income) to be approximately 1.4. However, the Pareto coefficient for capital income is approximately 1.38, while the Pareto coefficient for labor income is approximately 1.6. Therefore, it was pointed out that capital income is more intensely biased to the super-rich class.

To some extent, it was possible to estimate the Pareto coefficient in relation to the income distribution including high-income earners in Japan by using tabulated data such as the Annual Statistics Report which has been published by the National Tax Agency. However, such estimation was not sufficiently accurate. In the past, estimates have been made using rankings of high-income earners and high taxpayers published in Japan. I estimated a Pareto coefficient of approximately 2.1 using rankings of high taxpayers in 2003. Afterwards, the ranking of high taxpayers was abolished in 2005 due in part to the enactment of the Act on the Protection of Personal Information. The growing income disparity has also been discussed in Japan in recent years. However, since academic use of tax data has not been approved, it has become difficult to conduct highly-accurate analysis of income distribution, including the sampling of the super-rich class.

Estimation of a Pareto coefficient based on tax data

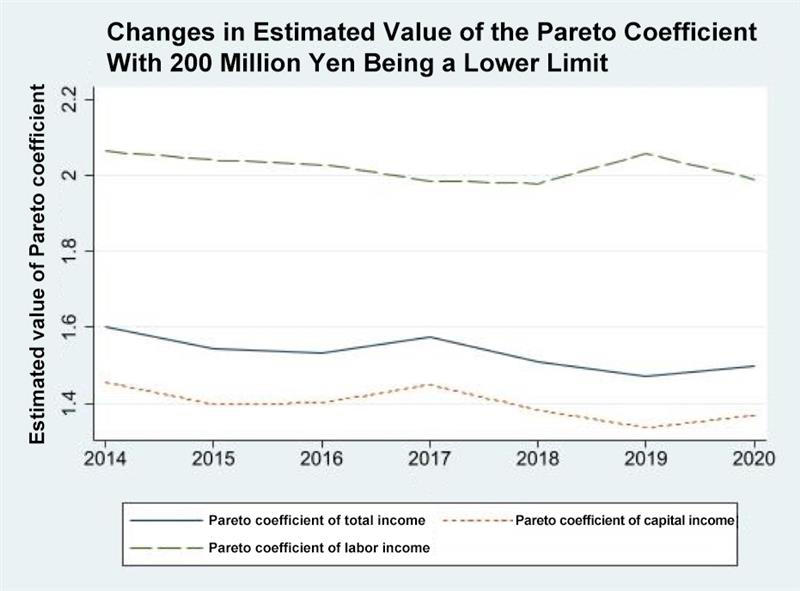

In the current joint research project, the data on income tax returns provided by the National Tax Agency contains the data of all persons with a total income of over 20 million yen. Currently, my research group is conducting analysis of income distribution by positioning taxpayers with a total income of over 20 million yen as high-income earners. A portion of our results are summarized in the National Tax College discussion paper which I co-authored with Yasutaka Yoneda of the National Tax College (currently a Specially-appointed Associate Professor at Tokyo Metropolitan University). The figure below shows a part of the discussion paper explaining changes in the estimated values of the Pareto coefficients from 2014 to 2020 for capital income, labor income, and total income with 200 million yen being a lower limit. The Pareto coefficients for total income and capital income were around 1.5 and 1.35, respectively, but have been trending downward during the period from 2014 to 2020. In contrast, the Pareto coefficient for labor income has been around 2 with no clear trend.

(Source: Kunieda and Yoneda (2023))

Although it is difficult to make a simple comparison due to the use of different data, the Pareto coefficient for total income that was estimated in our current research is extremely low compared to estimated Pareto coefficients for Japan in the past (for example, I estimated a coefficient of 2.1 in 2003). This indicates that income concentration in the super-rich class has progressed in Japan. The Pareto coefficient for total income is close to the Pareto coefficient for capital income. It is inferred that a factor behind the concentration of income is income concentration of capital income in the super-rich class. This is similar to the situation in the United States. Some instances of past research have focused only on labor income and claimed that the income disparity in Japan has not grown significantly. However, our analysis demonstrates that the income disparity analysis that is not based on data including financial income can be misleading.

In relation to the income tax system, the Tax Commission of the Japanese government has pointed out the existence of the "100 million yen wall." This refers to how the income tax burden on high-income earners decreases because a high proportion of their income consists of income to which separation tax on financial income, etc., is applied. Taxation of financial income is important in order to correct the widening of income disparity due to the concentration of financial income in the super-rich class.

Future research

As described above, research using income tax return data provided for the first time by the National Tax Agency has revealed that the concentration of income in the super-rich class is progressing in Japan. Our research group is studying topics such as the elasticity of taxable income, which examines how taxable income responds to changes in tax rates, and the redistribution effects of the income tax system. With the estimation of the Pareto coefficient and elasticity of taxable income in the income distribution of high-income earners, it is theoretically possible to drive the optimal income tax structure in Japan. Through future research, I will work to clarify the optimal income tax system in Japan.

(Reference Literature)

- Saez, E., and S. Stantcheva (2018). "A Simple Theory of Optimal Capital Taxation" Journal of Public Economics, Vol.162, pp.120 to 142

- Kunieda, S. (2012). "New Optimal Income Tax Theory and Japan's Income Tax System" The Japanese Economy, 39 (4), pp.60-78

- Kunieda, S. and Yoneda, Y. (2023). "Significance of Analysis Based on Tax Data Related to the Japanese Income Tax System" National Tax College Discussion Paper Series 230100-01ST (https://www.nta.go.jp/about/organization/ntc/kyodokenkyu/kohyo/pdf/230100-01ST.pdf)

Shigeki Kunieda/Professor, Faculty of Law, Chuo University

Area of Specialization: Public Finance and MacroeconomicsShigeki Kunieda was born in Saitama Prefecture in 1962. He graduated from the Faculty of Economics, University of Tokyo in 1984. He joined the Ministry of Finance in the same year. He earned a Ph.D. in economics from Harvard University in 1989. After working as Assistant Professor at Osaka University and Associate Professor at Hitotsubashi University, he assumed his current position in 2018.

He researches a wide range of topics including tax systems, social security, and fiscal policy.

His main written works include Economic Analysis of Welfare (coauthored; won the Nikkei Prize for Excellent Books in Economic Science, 2008, University of Tokyo Press) and more.

- Share articles