Return to a "Appropriate and Positive Interest Rates"

ーInterpreted through the Lens of Monetary Theory

Sixth Collaborative Course with "Otemachi Academia"

Masashi Chikahiro/Associate Professor, Faculty of Economics, Chuo University

The speaker in this webinar is Mr. Masashi Chikahiro, an associate professor at Chuo University's Faculty of Economics.

He is a spirited economist specializing in money supply theory (money and banking theory). At the same time, his favorite pastime is piano and loves it enough to have built a piano studio dedicated to his pianos. His commitment to the piano led him to set up his own channel on YouTube, through which he streams his piano playing ("Chikahiro Piano").

His published works include contribution to "Abenomics-ka no Chihokeizai to Kinyu no Yakuwari (tentative translation: The Role of Local Economy and Finance under Abenomics" (Sotensha Publishing Company)

Bold monetary easing, which Japan introduced in 2013 as one of the pillars of Abenomics, had continued negative interest policy as a globally unprecedented during long time by Bank of Japan (BoJ). However, on March 19, 2024, at the press conference held after the Monetary Policy Meeting, BoJ governor Kazuo Ueda announced an end to the negative interest policy that had lasted for eight years. "The large-scale monetary easing policy has achieved its role," he said.

Before this announcement, this webinar "Otemachi Academia" collaborative course organized jointly by Chuo University and Yomiuri Newspaper was held on March 15. At this webinar, Mr. Chikahiro, a specialist in monetary theory, offered his own interpretation of the transition in BoJ's monetary policy.

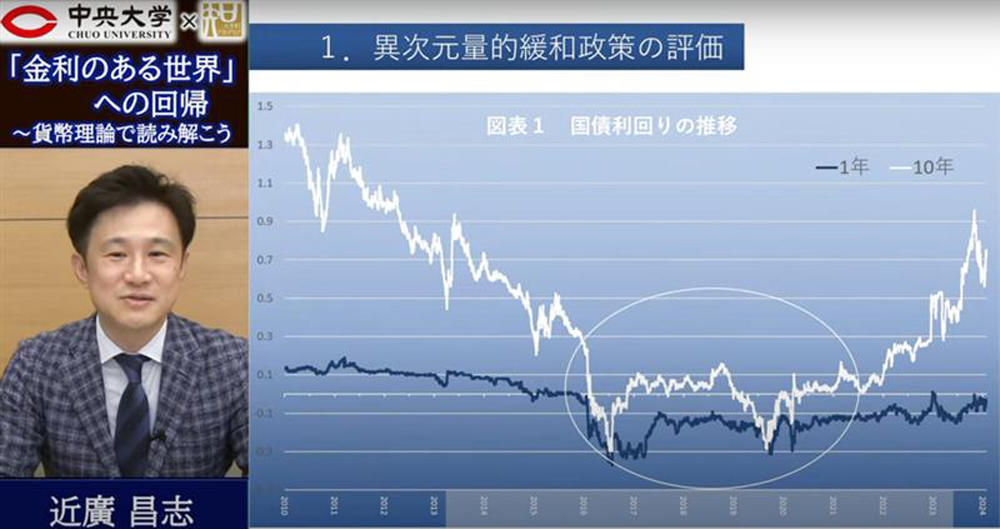

Evaluation of the Bold Quantitative Monetary Easing Policy

It is commonly said that the bold quantitative monetary easing policy was introduced by Haruhiko Kuroda, who became governor of the BoJ in March, 2013, immediately after he assumed the position. However, the BoJ's policies before that were not necessarily conventional ones. Earlier governor Masaru Hayami took drastic policies as well, deciding to introduce the zero-interest rate policy in 1999. Mr.Hayami also introduced quantitative easing policies in 2001, which were unprecedented tries (policy means) in Japan. Masaaki Shirakawa, Kuroda's immediate predecessor, also took drastic policies, such as setting up special "purpose fund to buy assets" in 2010, to promote the monetary policy of quantitative easing.

During this period, Japan was a "world without interest rates." Japan's interest rate policy changed from a zero-interest rate policy to a negative-interest rate policy, but the review and reputation is yet to be established. Successive BoJ governors have tried many approaches, which is highly appreciated.

Since the period of zero-interest rate policy, there were no profits from call-market or call-rates, and the absence of call-loan lenders made the short-term money market dysfunctional. Then, after the negative-interest rate policy was introduced, the deposit and loan margin of commercial banks have shrank, making banks' management difficult. However, even if "negative-interest rates" were adopted, not all short-term interest rates became negative; rather, the interest rates that became negative were very limited. Still, it made operating the pension funds difficult and posed the possibility of future loss on the BoJ due to trust issues.

On the other hand, there were advantages and benefits as well. The lower interest rate on government bonds eased the burden on the Ministry of Finance. However, buying major or public/listed companies' stocks to stabilize their stock prices or market value is not the radical role of the BoJ.

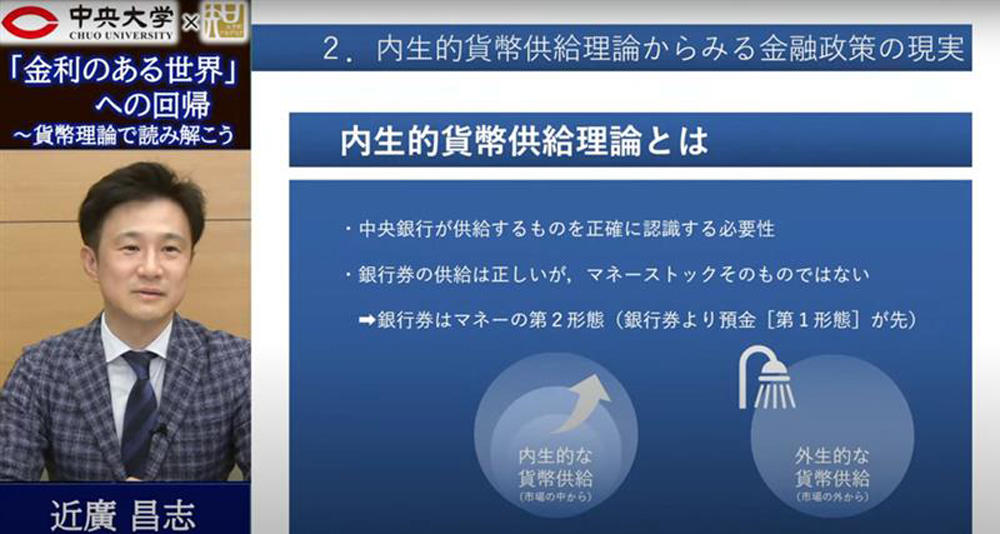

The Reality of Monetary Policy from the Perspective of Endogenous Money Supply Theory

As the word "endogenous" is difficult to use and explain, it may be better to say it another way: "emphasis on reality-oriented." That is, what corporations such as commercial banks and securities companies (brokers) are thinking, operates and functions at the frontlines.

I believe banknotes are the secondary form of money and that deposits as banks' liability are the primary form. While it is correct that the BoJ' have the role and its function is to supply banknotes, that does not mean money stock itself.

If I want to build a factory, I will apply for a loan from a bank and I get a loan. At this time, the bank create deposit as its own liability(debt). The bank's balance sheet expands both-side, loan (lending balance) assets and deposit liabilities. It is not only the loan side that increases. Always consider under the balance sheet (principles of book-keeping).

My seminar (Chikahiro Seminar, CHUO University) creates and sells its own original LINE-Stamps that say "Society runs on the bookkeeping principle and kindness." The bookkeeping principle is important in all we do.

It is a mistake and incorrect to believe that central banks can control the balance of money circulating in the country. In reality, a call market exists among commercial banks. What a central bank can do is guide the over-night interest rates on the call market (call rate) by buying or selling government bonds (operations). However, a central bank has no function to directly control the quantity of money of private sector (money stock), and we need to understand that a central bank should not directly control the amount of money. What is very important is that the creation of money is creation of deposits through loans originating from the demand for borrowing by the private sector. This is a role of commercial banks.

How to Perceive the Current Hot Topic of Monetary Theory

While I do not deny everything about MMT (Modern Monetary Theory), which some people are supportive, this theory contains risky aspects. Major advocators of MMT are U.S. economist L. Randall Wray and U.S. politician Stephanie Kelton among others. The theory says that the money, which is a private asset, is a debt of the money issuer, and that the quantity of money should be increased until the unemployment rate reaches low level.

The ultimate point of this theory is integrated government. The underlying theory of MMT is the same as "hansatsu (government note)," money issued by feudal domains during the Edo Period in Japan. The aim is to control money stock through integration of the government and a central bank. MMT proponents claim it is a "modern" monetary theory, but in truth it is a throwback to feudal times.

The hansatsu system ultimately came apart due to the collapse of the money's value, so the Meiji Government established a central bank independent of the government. Article 5 of the Public Finance Act sets out that the BoJ is prohibited from lending or supplying credit to the government and government bonds, so in principle BoJ underwrites government bonds by private financial institutions.

The value of separating central banks and governments was recognized in Europe two centuries ago and the practice has been preserved since then. This is a testament to human wisdom.

Likewise, keeping the BoJ's independence from government is crucial.

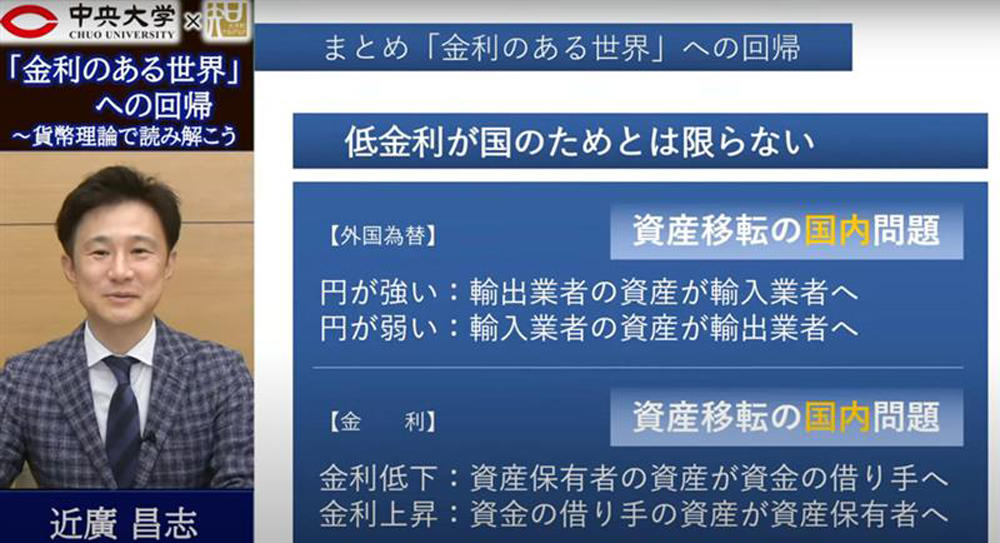

What will Happen in a "World with Interest Rates"?

Bold quantitative monetary easing has both advantages and drawbacks. Let me point out some of the advantages. For one, it taught us that we cannot do what we cannot do, and to define the theory more clearly. One result of Japan having a lower policy interest rate than other countries is a relatively weaker yen, which rather positioned that as a channel strategy during the period of bold monetary easing by BoJ. Intervention in foreign exchange markets is a task of the Ministry of Finance; it is not in the BoJ's task to intentionally keep stock prices high or maintain them.

Yet there are many problems associated with abnormally low interest rates. One is the possibility of destroying the market mechanism, and they help zombie companies that should have shut down to survive. Furthermore, the weaker yen negatively affects the economy because it causes higher electricity and gasoline/energy prices. Still, our daily lives have not become that much worse, and I believe we have managed by applying plenty of wisdom.

Even if the BoJ raises interest rates out of negative range, I doubt there will be major changes in the long-term interest rate structure. As the world of interest rates is compound interest, there should be some influence. But when it comes to household budget, we do not need to be overly concerned about the interest burden on items such as mortgages and car loans as long as competition among commercial banks is functioning.

Although some people may worry or concern about the negative impact on the stock market, the flip side is that increasing the interest rate implies that Japan's economy is strong. This may cause stock prices to increase.

The story of economic conditions is very much a narrative, and cannot be determined only through factors like income and interest rates. Though many people forecast the yen to appreciate to the other currencies, but we don't know that either. And the yen's strength or weakness is primarily a domestic issue. When the yen appreciates, domestic money earned by companies that have been profitable through exports when the yen was weak will only shift to companies making profits through importing.

The monetary system and clearing system is what supports our lives, and shaking this system could lead to disaster. Although negative interest rates offered some benefits, they also played a part in destroying markets, so I think it is necessary to raise or normalize policy rates as soon as possible.

* Click here for the video of the special dialogue held during the sixth collaborative course with Otemachi Academia on March 15, 2024, titled Return to a "World with Interest Rates"--Interpreted through the Lens of Monetary Theory.

Masashi Chikahiro/Associate Professor, Faculty of Economics, Chuo University

Born in 1978 in Kure City, Hiroshima Prefecture, he graduated from the Department of Banking and Corporate Finance, Faculty of Commerce at Chuo University. He completed his doctoral degree through the Graduate School of Commerce, Chuo University, and earning a Ph.D (monetary economics). Before taking his current position in 2022, he served as a lecturer and then associate professor at Faculty of Law and Letters of Ehime University.

His major published works include a contribution to Chapter 5 of "Kanritsukasei to Chuo Ginko (tentative translation: The Controlled Monetary System and the Central Bank" (Authored and edited by Takao Kamikawa and Yoichi Kawanami "Shinpan Gendai Kinyuron (tentative translation: New Modern Finance Theory), Yuhikaku Publishing Co., Ltd.